All Categories

Featured

Table of Contents

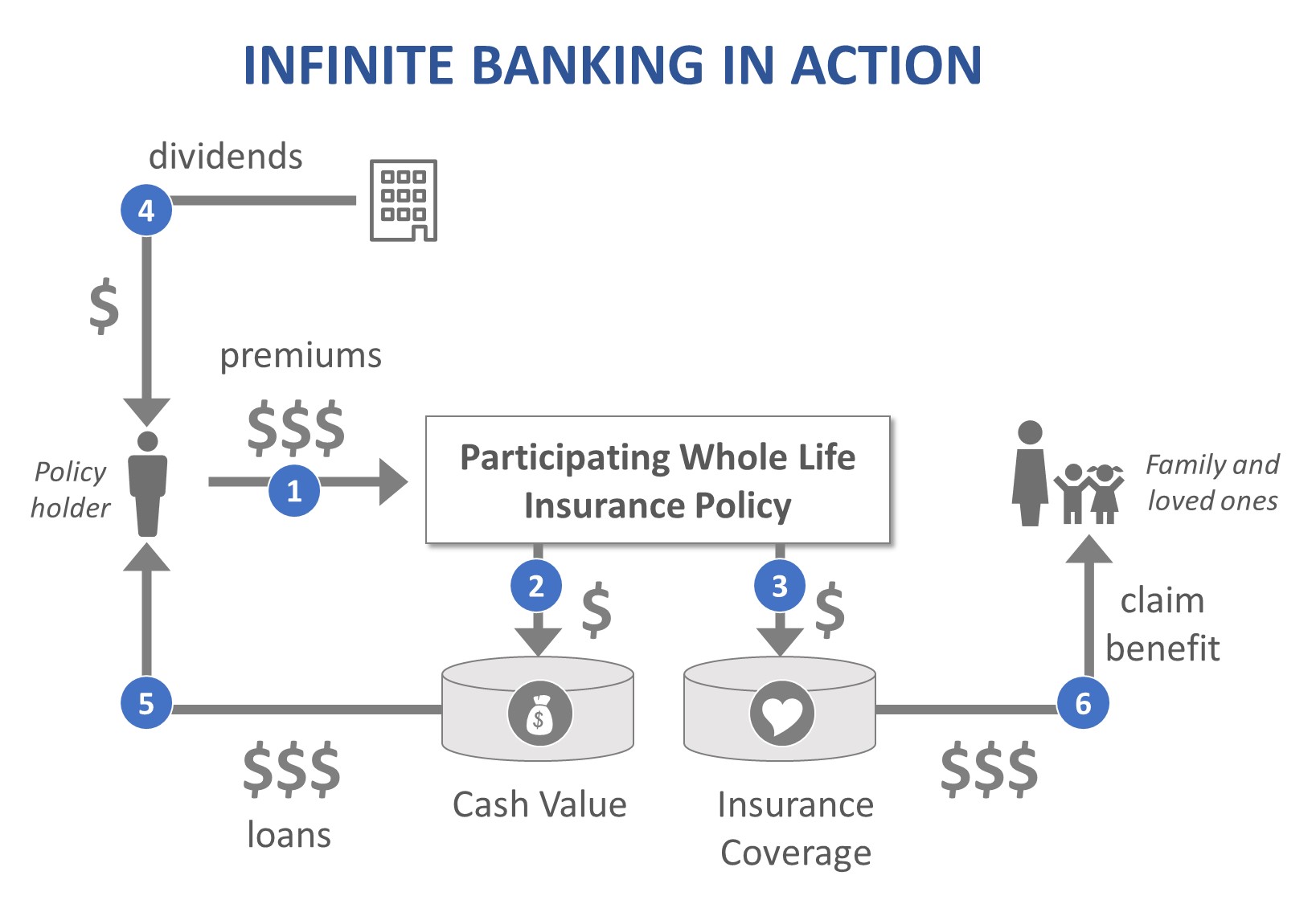

The are whole life insurance and universal life insurance coverage. The cash money worth is not added to the fatality advantage.

The policy loan interest price is 6%. Going this path, the interest he pays goes back right into his policy's cash worth rather of an economic establishment.

Infinite Banking Definition

Nash was a money expert and follower of the Austrian college of business economics, which advocates that the value of goods aren't clearly the outcome of traditional economic frameworks like supply and demand. Rather, individuals value cash and products in a different way based on their financial standing and demands.

One of the pitfalls of traditional banking, according to Nash, was high-interest rates on car loans. Long as banks established the interest prices and loan terms, individuals didn't have control over their very own riches.

Infinite Financial requires you to possess your monetary future. For goal-oriented individuals, it can be the most effective financial device ever. Below are the advantages of Infinite Financial: Perhaps the solitary most helpful facet of Infinite Banking is that it boosts your capital. You don't require to go with the hoops of a standard bank to obtain a car loan; just request a plan funding from your life insurance firm and funds will certainly be provided to you.

Dividend-paying entire life insurance is extremely reduced threat and uses you, the policyholder, an excellent offer of control. The control that Infinite Banking supplies can best be organized into 2 groups: tax obligation advantages and property securities - the infinite banking system. One of the factors entire life insurance policy is excellent for Infinite Financial is just how it's taxed.

Infinite Banking Uk

When you make use of entire life insurance policy for Infinite Banking, you become part of a personal agreement between you and your insurer. This privacy uses specific property defenses not found in other economic automobiles. These defenses may differ from state to state, they can include protection from possession searches and seizures, defense from reasonings and defense from financial institutions.

Whole life insurance policy plans are non-correlated properties. This is why they work so well as the financial structure of Infinite Banking. Despite what happens out there (supply, realty, or otherwise), your insurance plan keeps its well worth. A lot of individuals are missing this important volatility barrier that assists protect and grow wealth, instead splitting their cash into two containers: savings account and financial investments.

Market-based financial investments expand riches much quicker yet are subjected to market changes, making them naturally high-risk. What if there were a 3rd bucket that offered security but also modest, surefire returns? Whole life insurance coverage is that 3rd bucket. Not only is the rate of return on your entire life insurance plan assured, your death advantage and costs are likewise guaranteed.

This structure aligns perfectly with the principles of the Continuous Wide Range Technique. Infinite Financial allures to those looking for better monetary control. Here are its main benefits: Liquidity and ease of access: Plan fundings provide immediate accessibility to funds without the constraints of typical small business loan. Tax obligation performance: The cash money value expands tax-deferred, and plan financings are tax-free, making it a tax-efficient device for developing wealth.

Cut Bank Schools Infinite Campus

Property security: In many states, the cash value of life insurance policy is protected from financial institutions, adding an additional layer of monetary safety and security. While Infinite Banking has its benefits, it isn't a one-size-fits-all service, and it features significant downsides. Below's why it may not be the very best method: Infinite Financial often requires complex policy structuring, which can puzzle policyholders.

Imagine never ever having to worry about bank loans or high interest prices once again. That's the power of boundless banking life insurance.

There's no set financing term, and you have the flexibility to select the settlement timetable, which can be as leisurely as paying off the loan at the time of fatality. This adaptability encompasses the servicing of the financings, where you can choose interest-only payments, maintaining the loan equilibrium flat and convenient.

Holding money in an IUL fixed account being attributed interest can frequently be far better than holding the cash money on deposit at a bank.: You have actually always fantasized of opening your very own pastry shop. You can obtain from your IUL policy to cover the initial costs of leasing a space, acquiring devices, and hiring team.

Infinite Banker

Personal finances can be obtained from standard financial institutions and credit scores unions. Here are some bottom lines to consider. Bank card can supply a flexible way to obtain cash for very temporary durations. Obtaining cash on a credit rating card is usually really expensive with annual portion prices of interest (APR) frequently getting to 20% to 30% or more a year.

The tax obligation therapy of plan car loans can vary considerably relying on your nation of home and the specific regards to your IUL policy. In some regions, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, plan loans are generally tax-free, using a considerable advantage. In various other jurisdictions, there might be tax obligation effects to think about, such as prospective tax obligations on the car loan.

Term life insurance policy only supplies a death advantage, without any cash worth buildup. This suggests there's no cash worth to borrow versus. This article is authored by Carlton Crabbe, President of Funding permanently, a specialist in offering indexed global life insurance accounts. The information offered in this write-up is for instructional and informational objectives just and ought to not be interpreted as economic or financial investment suggestions.

Nevertheless, for lending policemans, the comprehensive policies enforced by the CFPB can be seen as difficult and limiting. First, lending officers typically suggest that the CFPB's laws produce unnecessary red tape, bring about more paperwork and slower lending handling. Policies like the TILA-RESPA Integrated Disclosure (TRID) regulation and the Ability-to-Repay (ATR) requirements, while intended at safeguarding customers, can lead to delays in shutting offers and enhanced functional costs.

{kind=link}

Table of Contents

Latest Posts

Ibc Personal Banking

Infinite Income System

Infinite Banking 101

More

Latest Posts

Ibc Personal Banking

Infinite Income System

Infinite Banking 101